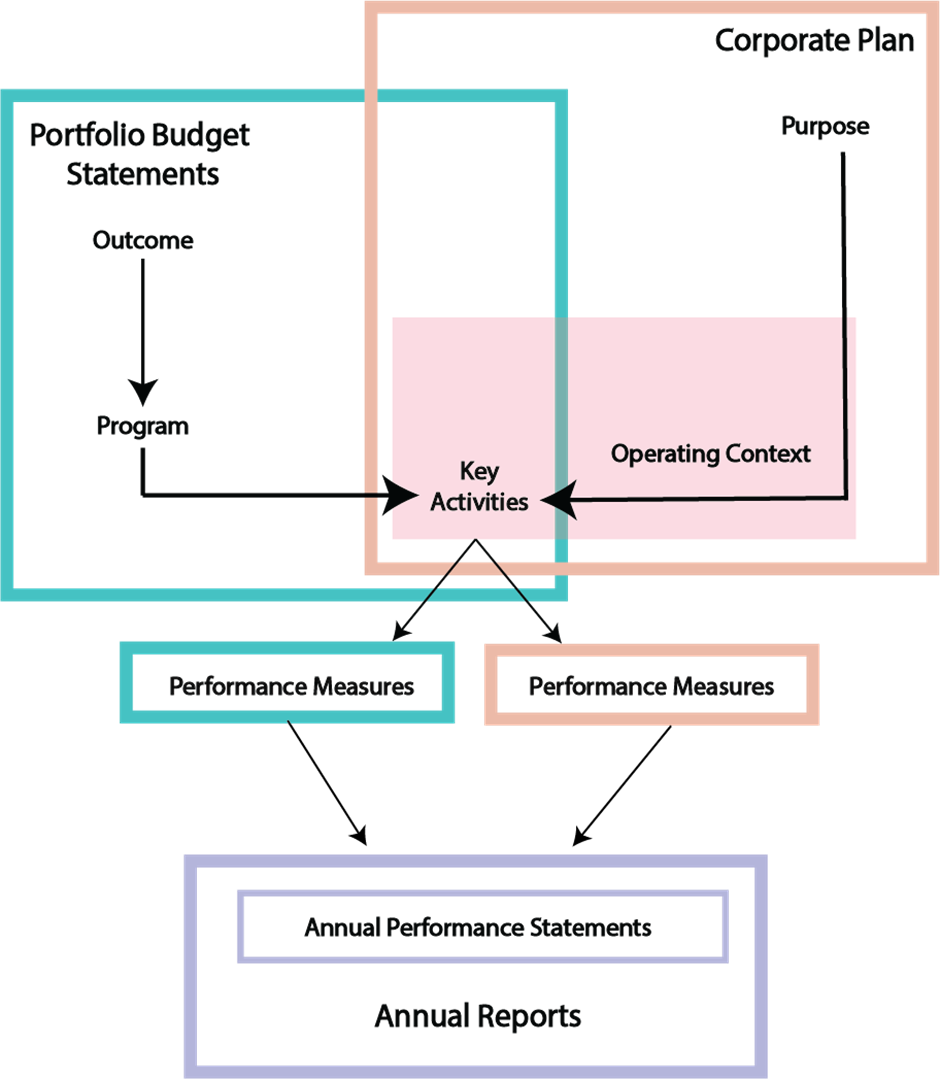

Relationship between the PBS and corporate plan

The reporting structure in Table 2.X.3 of the PBS, available under Tools and templates, displays the connection between an entity's outcomes, programs, related key activities (as expressed in the current corporate plan) and performance measures, including expected and planned performance results.

Key activities connect the PBS and corporate plan

The reporting of key activities provides the link between the PBS and the corporate plan. This linkage enables the reader to readily access the corporate plan to further understand the purposes of the entity and the operating context in which the key activities are undertaken, including:

- the environment in which the entity operates

- the capability needed to undertake the key activities

- the key risks that are managed and how they are managed

- who and how the entity cooperates with

- how any subsidiaries help the entity achieve the purposes.

The corporate plan, designed as the primary planning document for a Commonwealth entity, provides the full suite of performance measures for the entity to allow an understanding of how the entity intends to measure and assess the achievement of its purposes. This information is provided for a minimum 4-year period.

It is important to maintain a clear read between the PBS and corporate plan, including outlining any changes to performance information in the corresponding corporate plan. The corporate plan provides the capacity to provide more detail as to any changes and the reasons for the changes to performance information.

The Transparency Portal provides ease of access to the full suite of an entity’s performance measures and the related contextual detail as it contains publicly available corporate plans, PBS and annual reports.

For further information on corporate plans, see RMG-132 Corporate plans for Commonwealth entities

What is the ‘clear read’ principle?

The Commonwealth Resource Management Framework is designed to support an accountable and transparent public sector by providing the opportunity for judgements to be made on the performance of Commonwealth entities in achieving their purposes.

To assist readers to form a judgement, reporting by entities should provide a clear read between the allocation and use of public resources, and the results being achieved through activities undertaken with these resources.

The PGPA Rule (section 16F) requires the measurement and assessment of an entity’s performance in achieving their purposes to be reported in an entity’s annual performance statements (which is included in the annual report). This involves the reporting of performance information in accordance with methods set out in the entity’s corporate plan and PBS.

For more information on preparing annual performance statements, see RMG-134 Annual performance statements for Commonwealth entities.

‘Clear read’ linkages

The below image outlines the 'clear read' linkages across the PBS, corporate plan and annual performance statements which form part of the Commonwealth performance framework. As the image illustrates, key activities connect the PBS and corporate plan.