Public Governance, Performance and Accountability Rule 2014 section 16EA(a)

The performance measures meet this requirement when they relate directly to one or more of entity's purposes or key activities.

Performance measures are required for each reporting period covered by the plan (that is, a minimum of 4-years). Entities often demonstrate this coverage through specified targets, where reasonably practicable to set a target, for each of the reporting periods covered by the plan.

Each performance measure must relate directly to one or more of the entity’s purposes or key activities. That is, each performance measure should be linked, connected or aligned with one or more of the entity's purposes and/or key activities. Under the Public Governance, Performance and Accountability Act 2013, an entity's purposes include its objectives, functions or role of the entity (see section 8).

For example, for an entity with purposes relating to policing and national security, with a key activity relating to investigating serious crime, a performance measure might be expressed as:

- Percentage of cases before the court that result in conviction.

- Positive return on investment for investigation of crime.

Similarly, for an entity with purposes relating to regulation, and key activities relating to monitoring compliance and taking enforcement actions, performance measures might be expressed as:

- Level of compliance with [specific statutory obligations] by regulated entities.

- Proportion of decisions upheld upon review (potentially including a target set to reflect an agreed proportion).

By contrast, for an entity with purposes or key activities relating to the provision of policy advice to government on legal matters, readers may find it difficult to understand how measures such as ‘Number of visitors to the entity’ or ‘Investment in new technologies ($)’ relate to the entity’s purposes. There is no clear connection between these measures and the purposes or key activities of the entity. Further, it may be difficult for the entity to demonstrate its level of achievement against its purposes through such measures.

Using mapping and structural techniques in corporate plans

A clear way to illustrate the relationship between an entity's purposes, key activities and performance measures in the corporate plan is through mapping and structural techniques.

Better practice plans use both mapping and structural techniques to clearly illustrate the relationship between an entity’s purposes, key activities and performance measures.

Mapping techniques

Entities use mapping techniques in their corporate plan to illustrate the direct relationship between the purposes, key activities and each performance measure. The mapping is often illustrated within a plan on a page or in the performance section of the plan.

The hierarchical relationship between other elements within a corporate plan such as an entity’s strategies or priorities may also be mapped to an entity’s purposes, key activities and performance measures.

Better practice examples use mapping techniques to clearly illustrate how each of the other elements directly relate individually to an entity’s purposes, key activities and performance measures, rather than collectively.

Examples

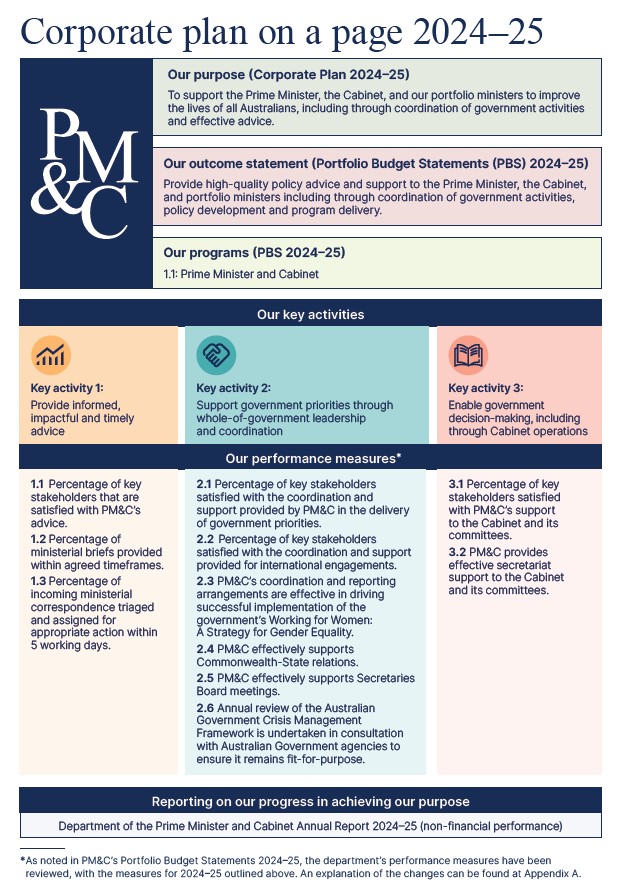

2024–25 Department of the Prime Minister and Cabinet Corporate Plan (page 4)

The Department of the Prime Minister and Cabinet uses mapping techniques within its a plan on a page to illustrate how each performance measure maps directly to each of its 3 key activities. The plan on a page also features its purpose, outcome statement and program.

Source: Department of the Prime Minister and Cabinet, Corporate Plan 2024–25, © Commonwealth of Australia

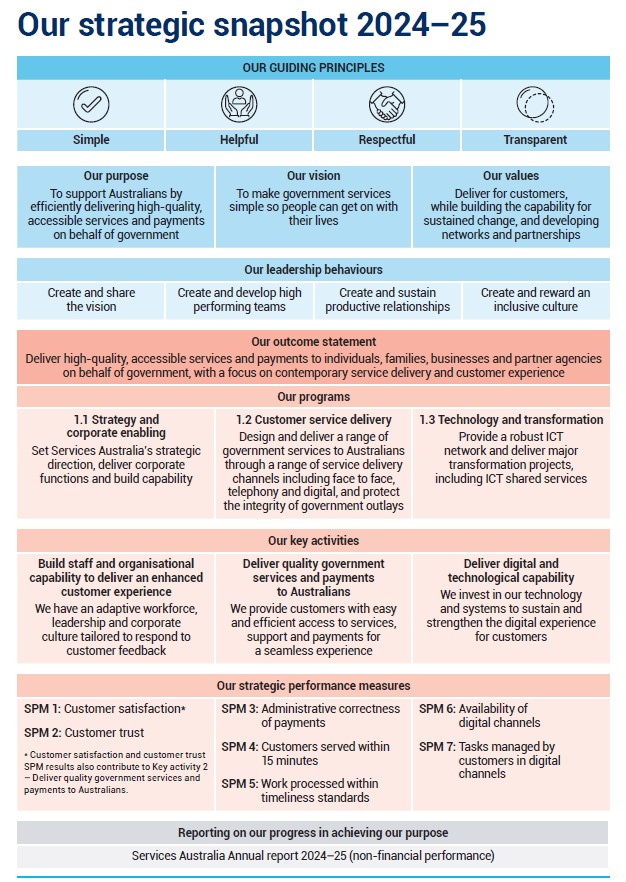

2024–25 Services Australia Corporate Plan (page 6)

Services Australia uses mapping techniques within its strategic snapshot (plan on a page) to illustrate how each performance measure maps directly to each of its 3 programs and 3 key activities. The snapshot also outlines its purpose and outcome statement.

Source: © Commonwealth of Australia (Services Australia) 2024

Structural techniques

The majority of entities use structural techniques in the performance section of the corporate plan to illustrate how each performance measure directly relates to their purposes and/or key activities. The plans structure the performance measures directly under the relevant purposes and/or key activities. This presentation provides the reader with a clear understanding of how each performance measure directly relates to an entity's purposes and/or key activities, often supported by narrative that provides context.

Examples

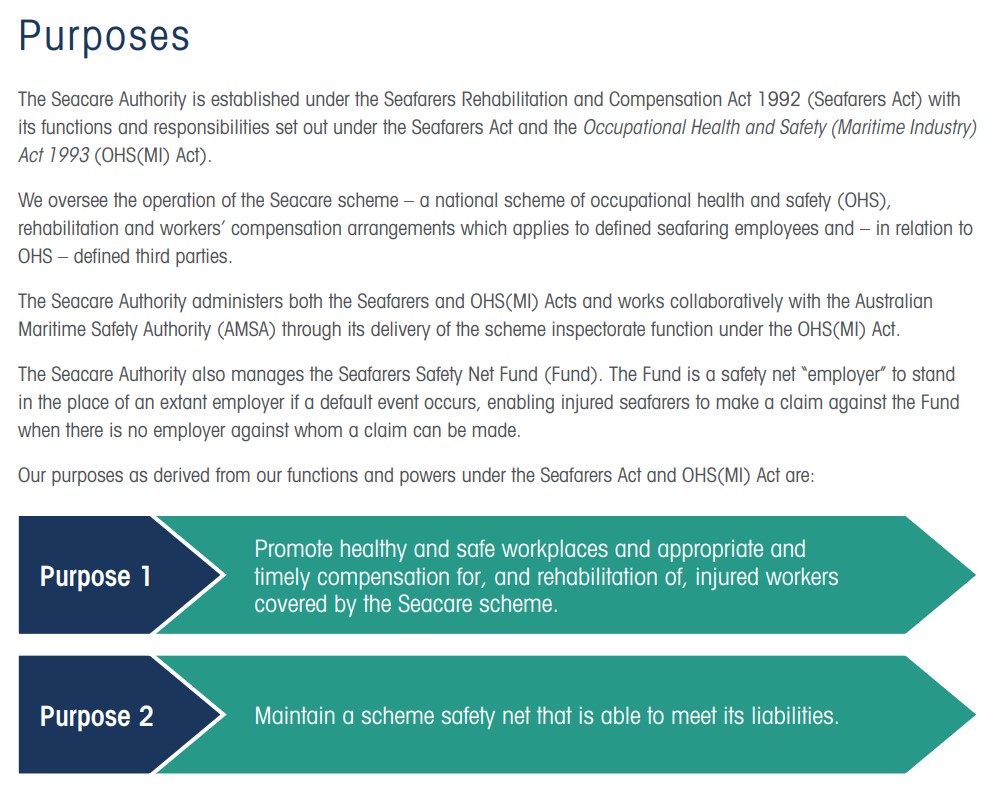

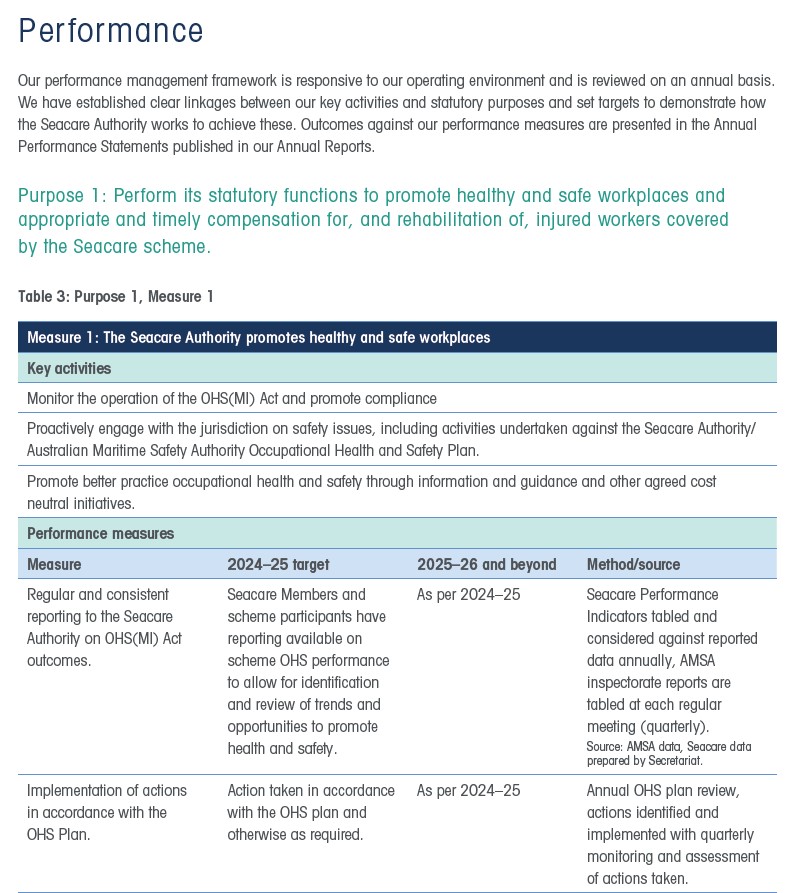

2024–25 Seafarers Safety, Rehabilitation and Compensation Authority Corporate Plan (pages 3 and 10)

The Seafarers Safety, Rehabilitation and Compensation Authority uses structural techniques in the performance section of its corporate plan to clearly illustrate how its performance measures directly relate to each of the entity’s purposes and key activities. This approach is typically adopted by entities with multiple purposes, where an individual performance measure directly relates to multiple key activities. For example, Measure 1 below directly relates to Purpose 1 and multiple key activities.

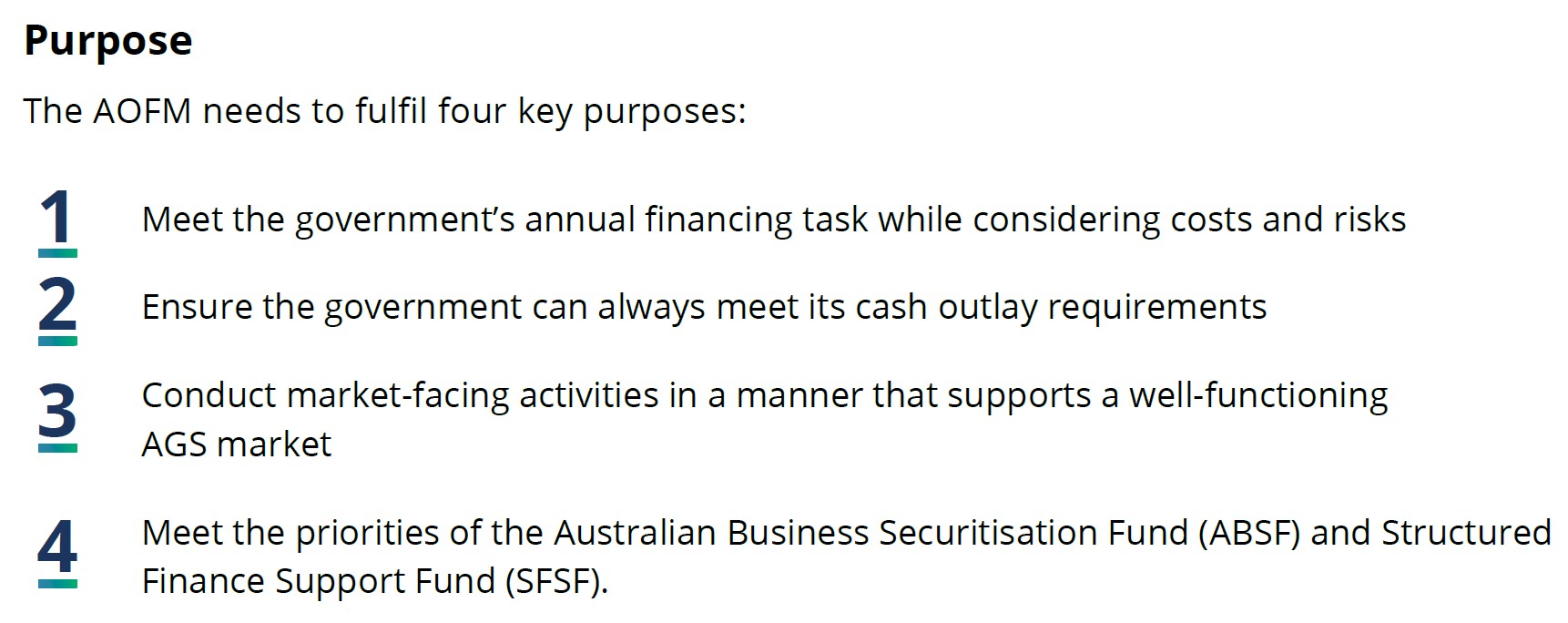

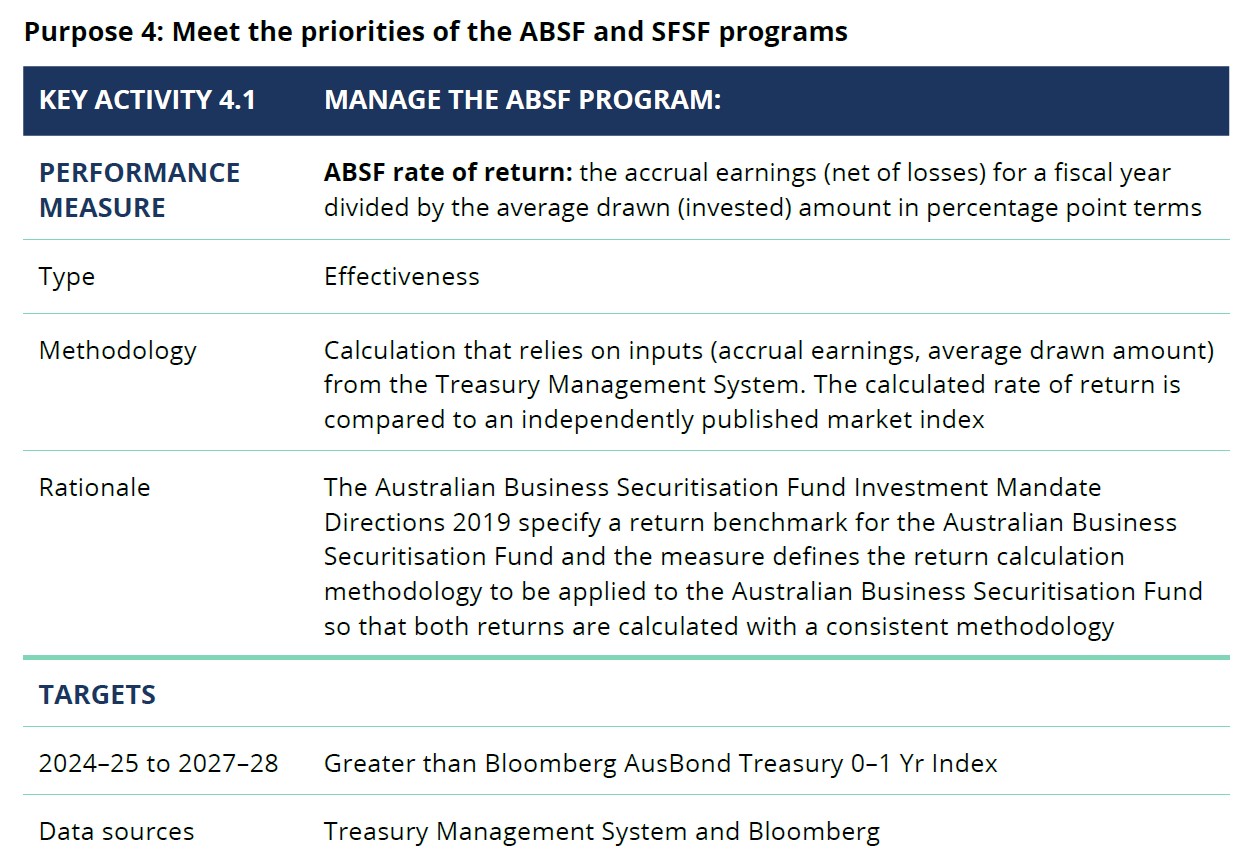

2024–25 Australian Office of Financial Management Corporate Plan (pages 6 and 15)

The Australian Office of Financial Management uses structural techniques in the performance section of its corporate plan to clearly illustrate how its performance measures relate to each of its purposes and key activities. This approach is typically adopted by entities with multiple purposes, where individual performance measures directly relate to individual key activities. For example, the performance measure below directly relates to Purpose 4 and Key activity 4.1.

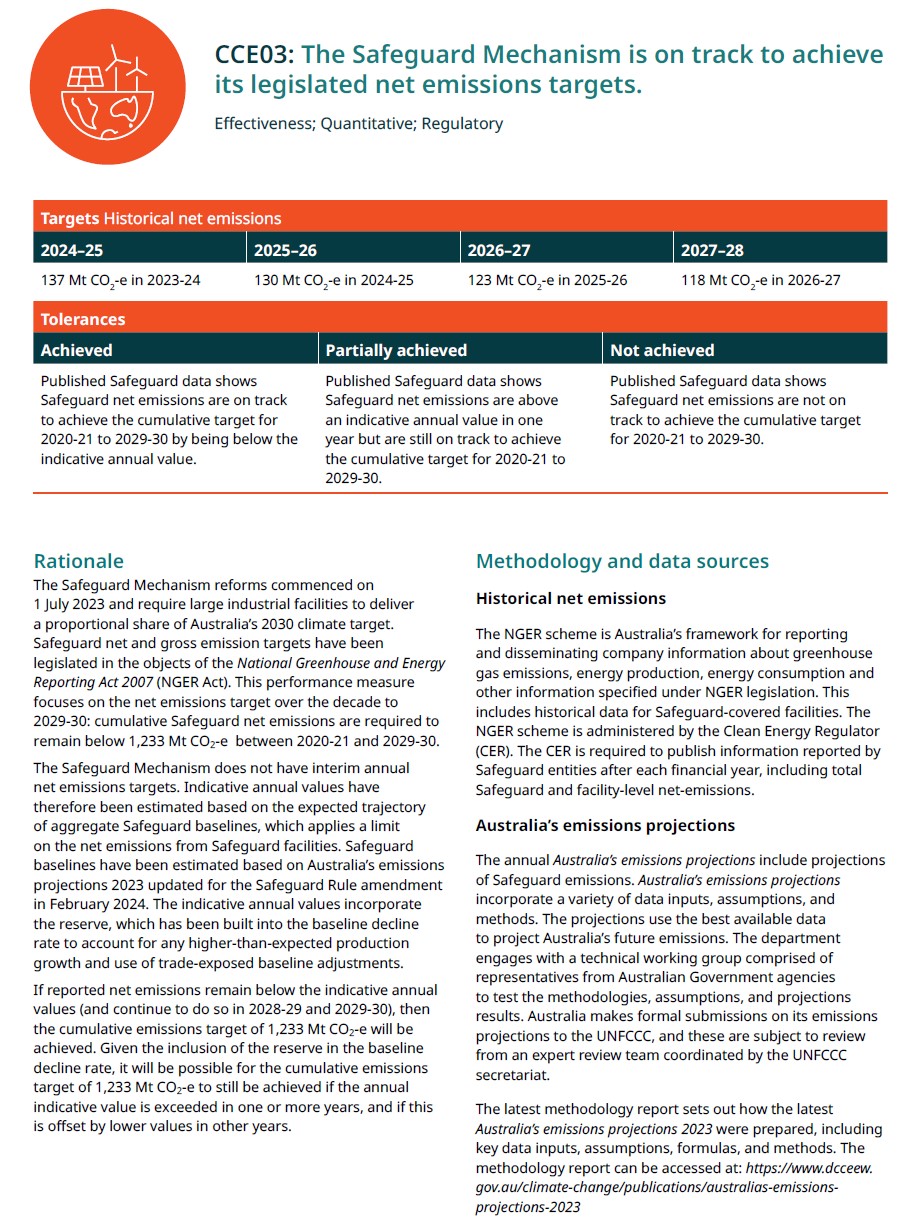

2024–25 Department of Climate Change, Energy, the Environment and Water Corporate Plan (pages 32 and 35-36)

The Department of Climate Change, Energy, the Environment and Water uses structural techniques in the performance section of its corporate plan to demonstrate how the performance measures relate to each outcome statement and the key activities. For example, Performance measure CCE03 below directly relates to Outcome 1 and Key activity 1.1. This approach is typically adopted by entities with a single purpose statement.

Source: DCCEEW 2024, Department of Climate Change, Energy, the Environment and Water Corporate Plan 2024–25, Department of Climate Change, Energy, the Environment and Water, Canberra. CC BY 4.0

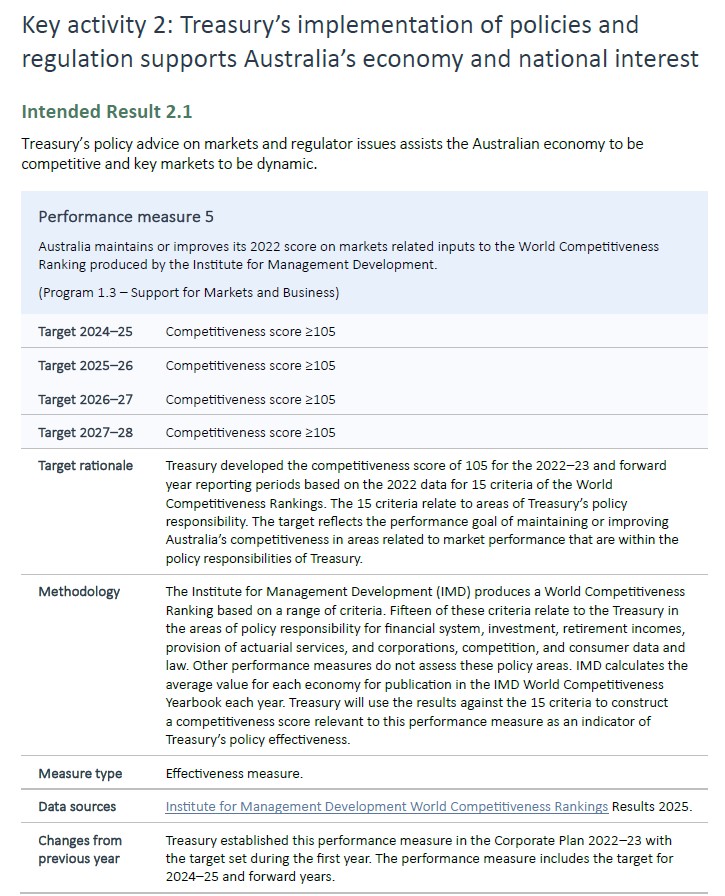

2024–25 Department of the Treasury Corporate Plan (page 16)

The Department of the Treasury uses structural techniques in the performance section of its corporate plan to demonstrate how the performance measure relates to its key activities. For example, Performance measure 5 below directly relates to Key activity 2. This approach is typically adopted by entities with a single purpose statement.

Contributing to achieving common objectives

Many Commonwealth responsibilities and activities involve contributing to achieving common objectives across the Commonwealth, with other jurisdictions, international partners and other parties such as the not-for-profit sector.

In these circumstances it can be difficult for an entity to report a direct ‘attribution’ towards the achievement of a common objective. Performance measures can be designed to explain the contribution the entity makes towards achieving common objectives.

For example, for entities whose purposes and/or key activities relate to the Closing the Gap priority reforms or national socio-economic targets, their performance measures may measure improvements in areas such as health, education, employment, housing, safety, culture and decision-making. The common objective is Closing the Gap.

Similarly, an entity whose purposes relate to national security and key activities relate to counter-intelligence, its performance measures may measure the impact of the policy advice it provides to key stakeholders has on their policy development and responses to threats. The common objective is the response to security threats.

Better practice examples clearly explain the contribution other entities make towards achieving common objectives and who they work with to achieve their results.

Examples

Entities often do this by outlining the respective responsibilities of other entities who contribute to their performance outcomes within the performance measures as demonstrated in the examples below.

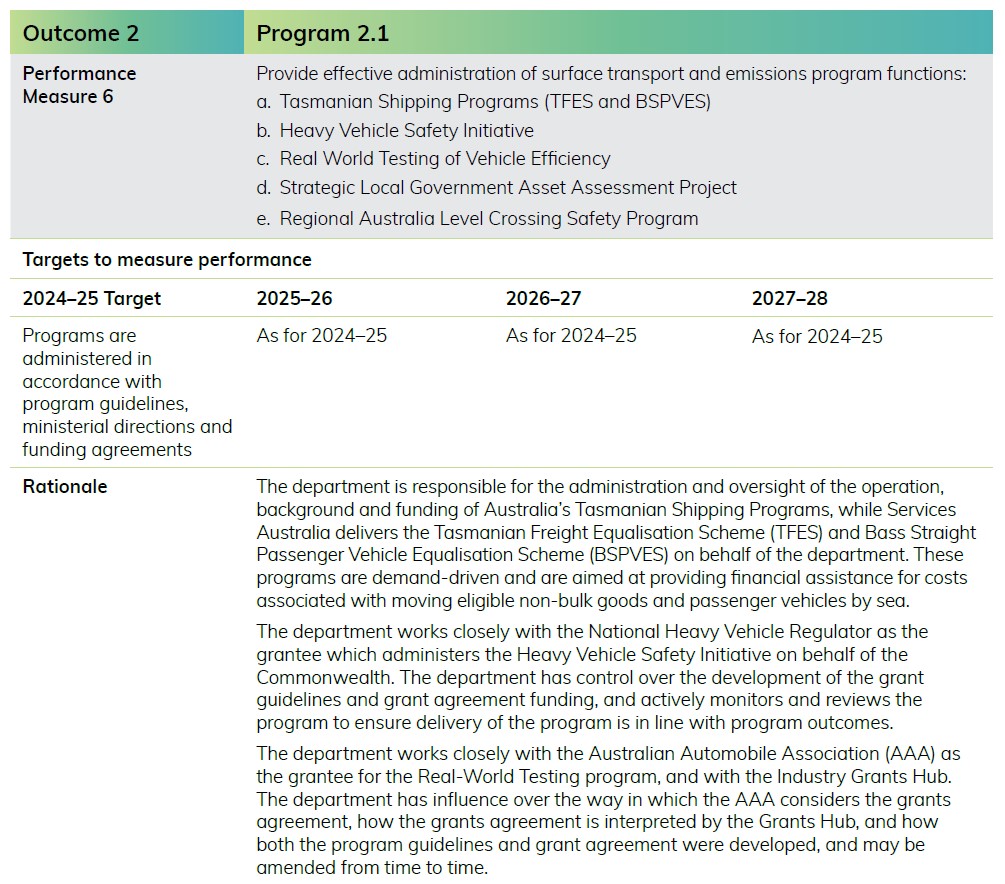

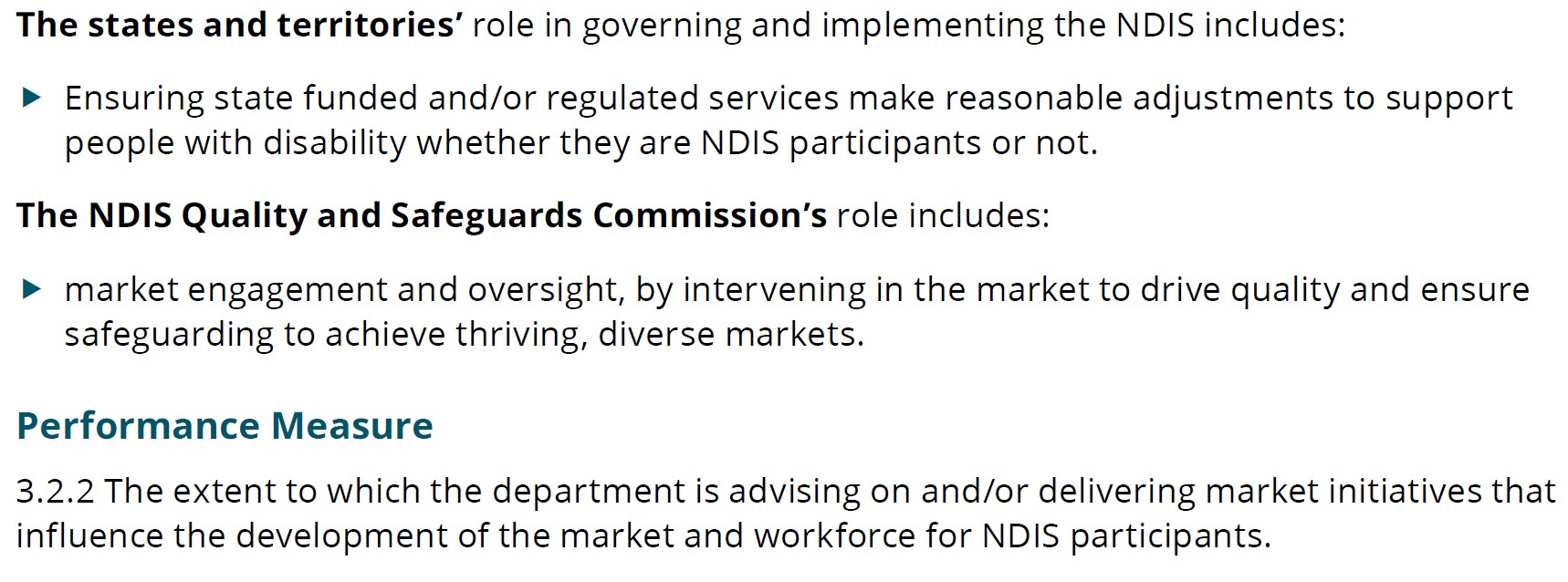

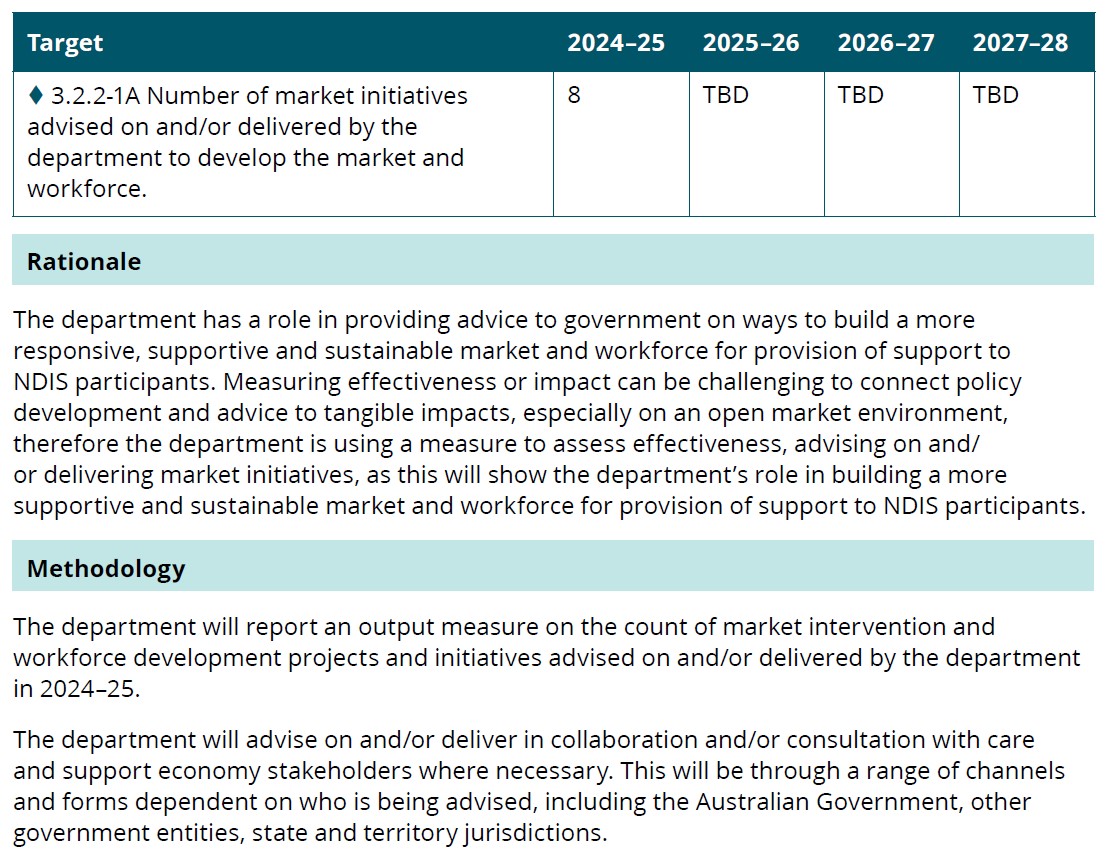

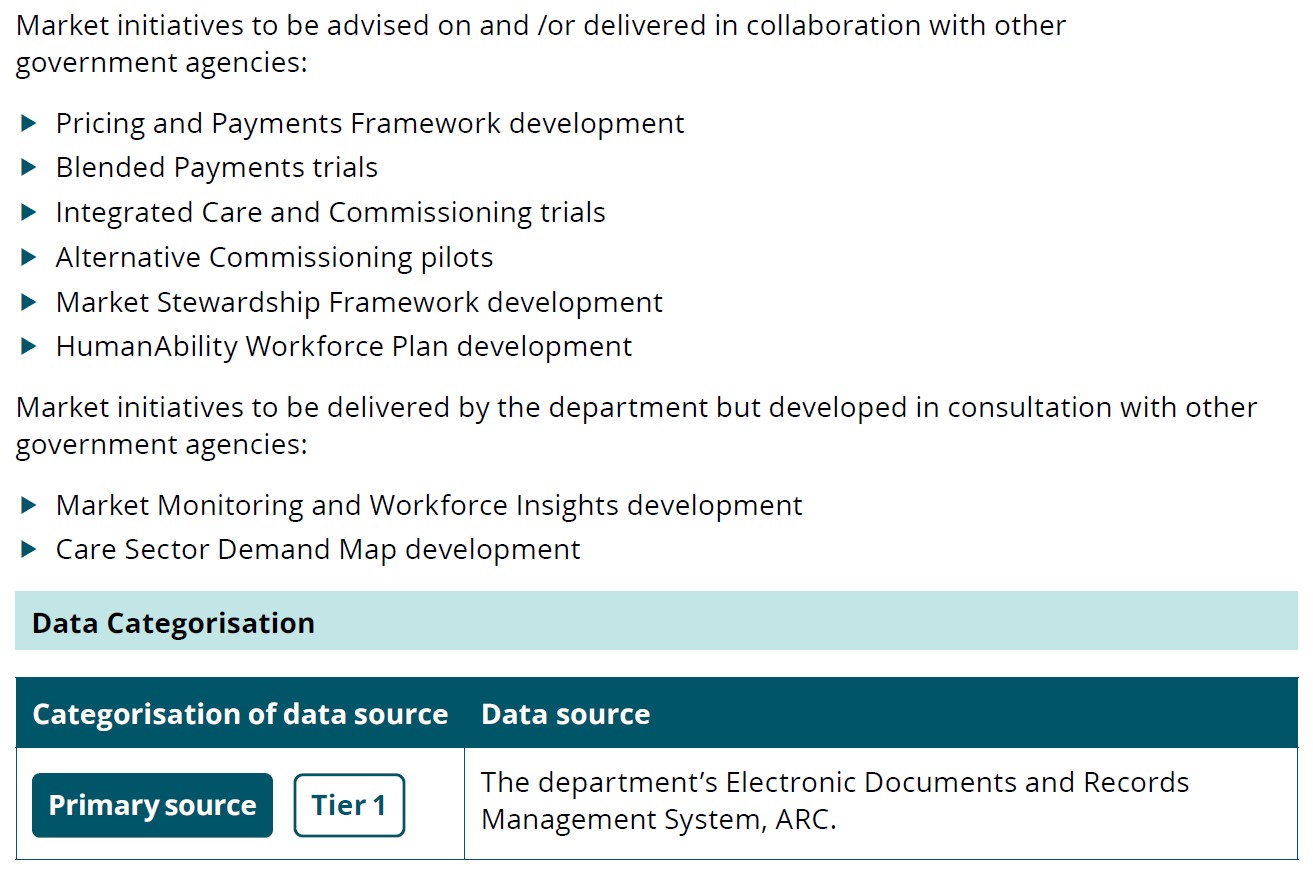

2024–25 Department of Social Services Corporate Plan (pages 69-70)

Source: Commonwealth of Australia (Department of Social Services)